Can Anything Challenge Ashburn?

For years, Ashburn, Virginia — the beating heart of “Data Center Alley” — has held the undisputed title as the global data center capital. With the highest fiber density in the U.S., close proximity to federal government agencies, and a robust cloud ecosystem led by Amazon Web Services, Ashburn has long dominated the colocation and hyperscale market.

But in 2025, the digital landscape is beginning to shift. Faced with mounting challenges such as power grid saturation, soaring land costs, and increased environmental scrutiny, hyperscale developers and colocation providers are actively scouting new territory. These next-generation locations — often found in Tier 2 and Tier 3 metros — are becoming hotbeds for data center investment.

This article dives into the factors fueling this decentralization and highlights the rising stars that could soon rival Ashburn’s dominance. We’ll also explore what this transition means for hyperscalers, developers, enterprises, and the future of digital infrastructure.

Why the Shift Is Happening

Power Bottlenecks in Tier 1 Markets

Traditional Tier 1 data center markets like Ashburn, Santa Clara, and Northern Virginia are facing power saturation. Utility companies are struggling to keep up with the intense demands of hyperscale data centers, which often require 100MW to 300MW of power per campus. Delays in substation construction, grid interconnection approvals, and prioritization of residential or industrial energy needs over data centers have created significant roadblocks. These constraints are pushing providers to search for locations with more reliable and scalable energy solutions.

Exploding Land and Real Estate Costs

Ashburn’s real estate market has become prohibitively expensive for new development. The cost of land has doubled over the last five years, now averaging between $2 million and $4 million per acre. By comparison, land in cities like Columbus, Reno, or Amarillo is significantly more affordable. Lower land costs allow developers to build larger campuses, plan long-term expansion phases, and offer competitive rates to clients. For hyperscalers aiming to deploy capital efficiently, these emerging markets are much more attractive.

Changing Latency Demands

As digital infrastructure becomes more decentralized, the need for ultra-low latency from core Tier 1 markets is shifting. Edge computing, content delivery networks (CDNs), AI inference, and streaming services often perform just as well in Tier 2 or Tier 3 metros, provided latency remains under 50 milliseconds. This evolution is enabling data center operators to expand beyond the traditional hubs, bringing services closer to end users without sacrificing performance.

Sustainability and ESG Pressures

Environmental responsibility is now a core requirement for enterprises and providers alike. Investors, customers, and regulators are demanding sustainable operations. Many new cities are better positioned to meet these needs. They offer cleaner energy sources, space for on-site renewable installations, and less congested grids with lower carbon intensity. This shift allows operators to reduce Scope 2 emissions and enhance their ESG credentials while maintaining efficiency and scale.

Rising Stars: The Top Emerging Data Center Cities

Hillsboro, Oregon

Often called the “Ashburn of the West,” Hillsboro has rapidly become a major hub for hyperscale builds. Located outside of Portland, it offers subsea cable access to Asia-Pacific regions, reliable hydroelectric power, and supportive state-level tax policies. Amazon, QTS, and Stack Infrastructure have already established major campuses, and the market shows no signs of slowing down.

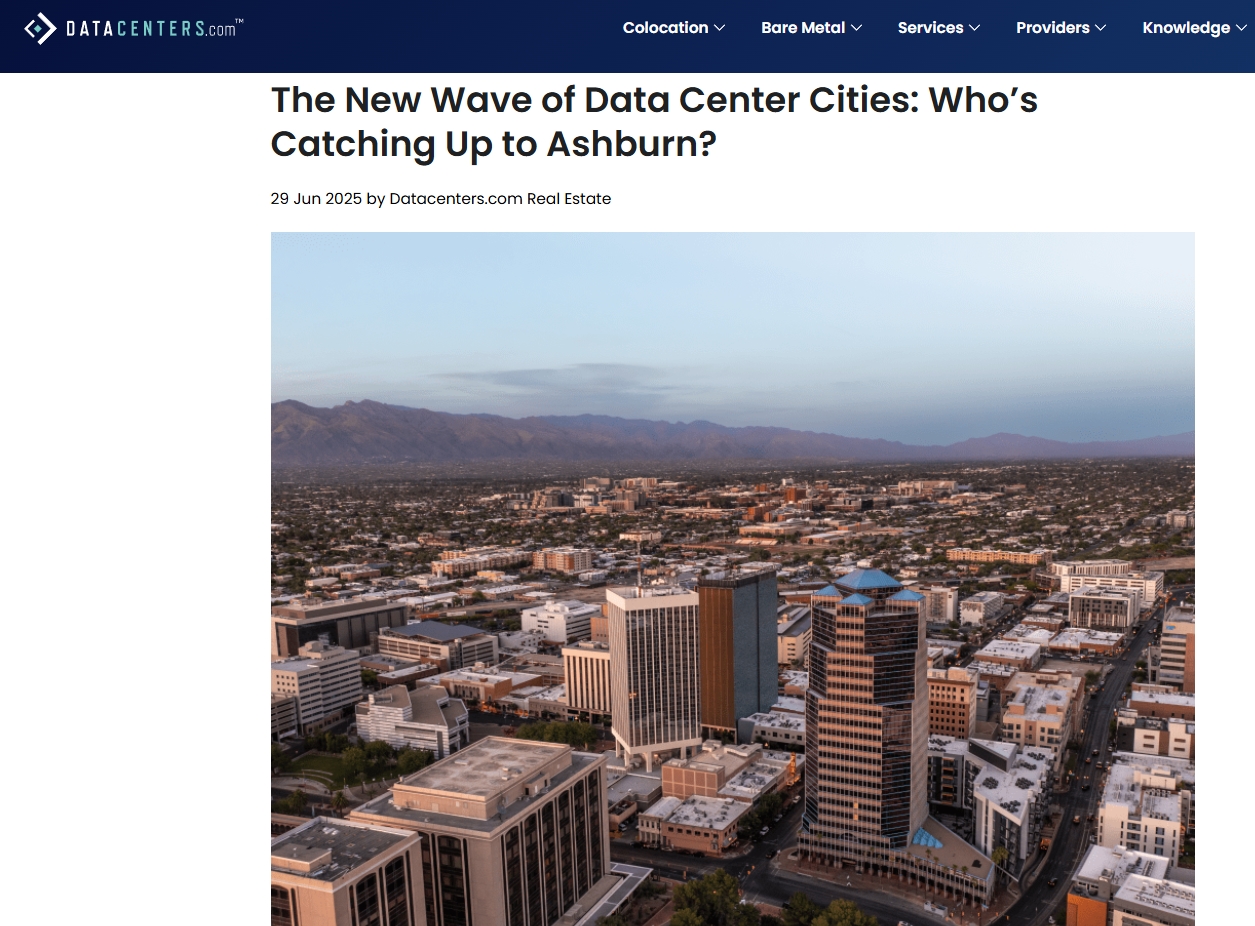

Phoenix, Arizona

Phoenix continues to rise due to its desert climate, affordable energy, and generous space for development. It's a region with minimal natural disaster risk and easy access to the massive Southern California market — without the burdens of strict California regulations. Providers like Aligned, Vantage, and Iron Mountain have invested heavily here, signaling long-term confidence in the metro’s viability.

Columbus, Ohio

Columbus is quickly becoming one of the most attractive U.S. locations for data centers. Hyperscalers including AWS, Google, and Meta have all made significant investments in central Ohio. The city’s location allows for balanced latency to both coasts, and strong partnerships with state institutions have created a pipeline of skilled talent and favorable business conditions.

Atlanta, Georgia

Already a telecommunications hub, Atlanta’s data center market continues to expand thanks to its strategic location, availability of long-haul fiber, and power reliability. Microsoft and Apple have made major announcements in the region, joining a growing list of providers that see Atlanta as a cornerstone of Southeast infrastructure strategy.

San Antonio, Texas

While often overshadowed by Dallas, San Antonio has seen an unexpected surge in data center development. Its access to the ERCOT grid offers energy independence, and local climate adaptation strategies have made cooling more efficient even during heat waves. Emerging designs such as modular and pre-cooled facilities have positioned San Antonio as a resilient alternative for hyperscale operations.

International Growth Markets

Johannesburg, South Africa

Johannesburg is becoming the central digital hub of Africa. Already home to AWS’s Africa region and Microsoft’s Azure cloud presence, it benefits from the expansion of major submarine cables like 2Africa and Equiano. Local providers such as Teraco are also scaling rapidly, tapping into both domestic and pan-African demand.

Madrid, Spain

Madrid has emerged as a Southern European alternative to the dense data center markets in Frankfurt and Amsterdam. It offers a cost-effective operating environment, lower power prices, and ample solar resources. Oracle, Google, and other providers have committed to building large campuses in the region.

Jakarta, Indonesia

Indonesia’s rapidly growing digital economy is driving data center expansion across the archipelago. Jakarta stands at the center of this growth, with hyperscalers investing in infrastructure to support rising demand from e-commerce, fintech, and mobile users. Government initiatives to improve connectivity and regulatory transparency are further accelerating development.

What Makes a City “Data Center Ready”?

To compete with Ashburn, a city must offer more than cheap land and tax breaks. Several key factors define a data center-ready location.

A robust power grid is foundational — data centers require massive and stable energy supplies, and outages are unacceptable. Climate resilience is equally important; data centers must maintain uptime in extreme weather and avoid cooling inefficiencies. Proximity to major fiber routes is critical for reducing latency and controlling bandwidth costs.

Favorable tax policies and development incentives help operators manage capital outlays, while skilled local labor ensures smooth construction, commissioning, and operations. Lastly, political stability and regulatory predictability make long-term investments feasible and secure.

When these elements align, a city becomes fertile ground for hyperscale and colocation success.

What This Shift Means for the Industry

For Hyperscalers

Major cloud providers are increasingly pursuing campus-style developments in remote regions where land and power are abundant. These builds require a higher degree of automation and remote management, especially for areas far from major cities. Partnerships with utilities, local governments, and energy developers are becoming essential.

Hyperscalers are also looking for cleaner energy and grid reliability as they align their infrastructure with global sustainability targets.

For Real Estate Developers

The growth of alternative markets is a boon for real estate developers. It enables them to secure land early, invest in critical infrastructure like water and energy access, and engage proactively with municipal planning departments. Developers can also work directly with economic development boards to ensure long-term zoning approvals and community buy-in.

For Colocation and Cloud Providers

These shifts create opportunities for providers to expand their go-to-market strategies. By deploying in secondary metros, they can offer lower-cost options, reduce latency for edge applications, and appeal to ESG-focused enterprises. Many are bundling compute, connectivity, and green energy offerings into unified service packages that appeal to distributed IT teams.

For Enterprises and Buyers

As more data center locations come online, buyers have more choices — and more leverage. The ability to deploy workloads outside of congested Tier 1 markets can lower costs and improve compliance with sustainability mandates. Enterprises can now design architectures that use regional nodes, follow-the-sun strategies, and multi-cloud environments without compromising performance.

Looking Ahead: Can Ashburn Hold Its Crown?

Ashburn remains a heavyweight in the global data center market. Its unmatched fiber density, robust cloud interconnects, and long-standing reputation will keep it at the top for years to come. However, its dominance is no longer unchallenged.

Power constraints, high real estate prices, and tighter regulatory oversight may cap its growth, giving way to a more distributed digital infrastructure ecosystem. Cities like Hillsboro, Phoenix, Columbus, and others are rising fast — and their trajectory suggests the future will be more balanced.

Ashburn will remain a vital core, but it is no longer the only core.

The Data Center Map Is Expanding

The decentralization of digital infrastructure is accelerating. From AI training clusters and edge computing to sustainability compliance and global connectivity, the next decade will see dozens of new cities emerge as data center leaders.

For developers, the time to identify and invest in these future corridors is now. For hyperscalers, flexibility and location diversity are becoming competitive advantages. And for buyers, the new wave of cities brings better pricing, more redundancy, and enhanced ESG alignment.

Ashburn’s legacy is secure — but the race is on. The next Ashburn may not look like the last one, and that’s a sign of a maturing, forward-thinking industry.